A micro company is a type of legal entity that complies with three cumulative conditions, as set forth by the legislation in force. The primary advantage of this business form is that, under certain circumstances, it can be subject to one of the lowest taxes for corporations in Romania.

| Quick Facts | |

|---|---|

| Romanian micro company qualification |

Turnover below EUR 500,000, owned by natural/legal persons other than the state and territorial administrative units, it is not subject to liquidation |

|

Minimum share capital for those who open a Romanian micro company |

No minimum share capital prescribed for the SRL |

|

Minimum number |

1 |

| Number of directors | Not mandatory for the SRL. It is managed by an administrator |

| Mandatory residency requirements | No |

| Local director required (Yes/No) to open a Romanian micro company |

No |

| Time frame for the incorporation (approx.) |

5-7 days |

| Corporate tax rate in Romania | 16% standard corporate income tax rate or 1%/3% of the revenue under the special micro company regime |

| Dividend tax rate | 8% |

| VAT rates in Romania | 19% standard rate 5% and 9% reduced rates |

| Number of double taxation treaties (approx. ) | 90 |

| Annual meeting required | Not applicable to the SRL, except as otherwise stipulated in the company’s constitutive documents |

| Accounting and filing requirements after you open a Romanian micro company | Quarterly corporate income tax payments. Annual financial statements. |

| Foreign-ownership allowed | Yes |

| Reasons to maintain the micro company regime in Romania | The micro tax is lower compared to the profits tax in Romania. Taxpayers can switch from one regime to the other if advantageous in their case, however, they may not switch back |

| 1% rate conditions | Applicable to businesses with a turnover below EUR 60,000. |

|

3% rate conditions |

For businesses with a turnover above EUR 60,000 or that engage in certain types of activities (as defined by their NACE codes). |

|

NACE codes for the 3% micro company regime (non-exhaustive list) |

5821, Computer game publishing activities; 6201, Custom software development activities; 6209, Other information technology service activities; 5510, Hotels and similar accommodation facilities; 5610, Restaurants, etc. |

| Switch from the 1% rate to the 3% rate | Starting with the quarter in which the company exceeds the EUR 60,000 threshold. |

| Switch from the 3% rate to the 1% rate |

Possible if, during the fiscal year, the turnover does not exceed EUR 60,000 or ceases to engage in certain types of activities (according to the NACE codes). |

| Special regime for hospitality (HORECA) companies |

Cannot qualify for the micro company regime starting with 2024 if they exceed the turnover threshold of EUR 500,000 (as was previously possible). |

| Conditions for the holding regime |

Limited to only one micro company (a holding of over 25% in a company is only possible for one micro company). |

| Types of companies that can qualify as a micro company |

Generally, the private limited company (SRL) |

| Micro-company regime when changing the business form |

Possible, if the new business meets the specified conditions. |

| Micro regime if the company does not have at least one employee | Not permitted |

| When does the micro company regime cease |

In the quarter in which the cumulative conditions are no longer met by the company. |

| Companies prohibited from adopting the micro company regime |

Examples include primarily those companies in the insurance and reinsurance sector. |

| Assistance for micro company creation in Romania |

Our team can provide assistance for investors looking to open an SRL company that will qualify as a micro company. |

| Services for micro companies offered by our team |

Assistance and counsel for meeting the ongoing requirements and complying with the latest fiscal changes. |

| When to contact us | As soon as you decide to set up a company in Romania. |

Many investors find that the micro company regime is a convenient one and one that allows for a simplified accounting practice. However, investors are advised to pay attention to all of the current regulations in force for this business form and fully understand its taxation regime, and the conditions under which it can change, before incorporating the new company.

Our agents who specialize in company formation in Romania answer some of the most common questions concerning this business form and can help investors incorporate a micro company. We provide complete pre and post-incorporation assistance to local and foreign company owners and our team of lawyers can also provide investors with the latest legislative changes that may concern taxation or different accounting and reporting requirements.

Investors who have more questions that those answered below about the micro company can reach out to our team of Romanian lawyers.

Question: I would like to open a small company in Romania. What does your Romanian law firm suggest?

Answer: Apart from the private limited liability company or the joint stock company, which are two of the most popular business forms, business people in Romania can also choose to register a micro company, which perfectly suits the needs of a small company pattern. A micro-company is a specific type of limited liability company which distinguishes from other business entities through several particular traits.

Question: What are the main steps for opening a micro company in Romania?

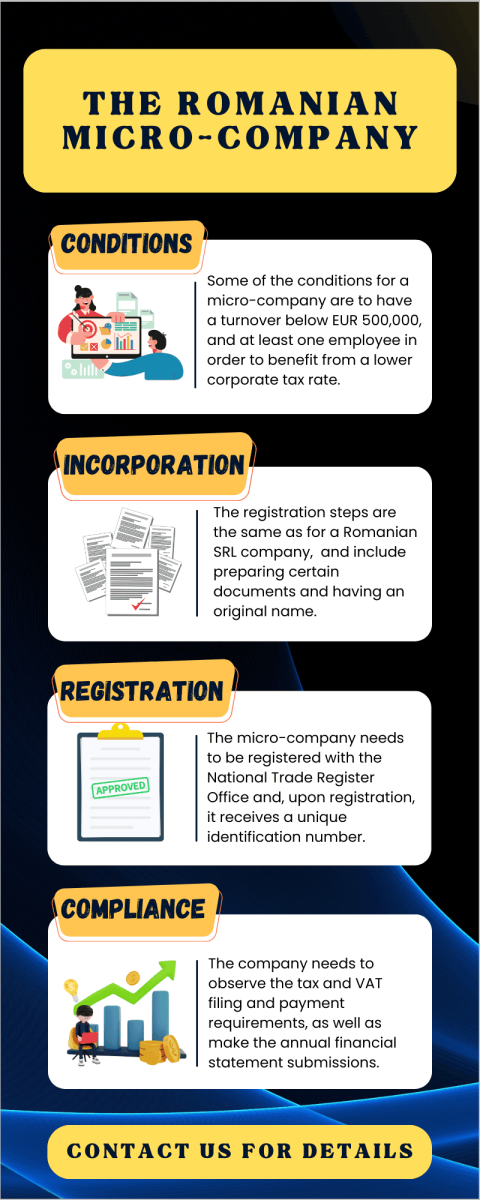

Opening a micro company in Romania comprises the same general steps required for the formation of other legal entities. These are listed below by our Romanian lawyers:

- Choosing a company name: this needs to be an original name that, once checked for availability, the name can be reserved.

- Drafting the documents: these are the Articles of Association and one of our lawyers in Romania can help you draft them.

- Open a bank account: the new company needs to have a corporate bank account.

- Preparing the documents: gathering all of the documents and filling in the registration application; the company directors will need to provide specimen signatures.

- Registering the company: the documents are submitted to the National Trade Register Office for the purpose of registering the new company.

The company’s Articles of Association include the following information about the company: the name and emblem, its registered office seat, the duration of the company and the type of company, the main business activity as well as the secondary ones, the names of the company administrators, the manner in which certain company modifications can take place. Our team can help entrepreneurs draw up the Articles of Association as well as provide the required assistance for correctly filling in the application form as well as any other needed forms when opening a micro company in Romania.

We recommend including more than one object of activity when incorporating the micro company in Romania. This is done according to the classification of the activities of the national economy and it is advisable to choose one main object and several other objects of activity as the process of adding more objects later will imply a number of steps and can be time-consuming for the company administrators. Company owners who wish to make subsequent changes to their company, such as adding more objects of activity or changing the company’s registered office can reach out to our lawyers in Romania.

Question: What are the characteristics of a Romanian micro company?

Answer: The former basic provisions imposed by the process of micro company registration in Romania clearly pointed out several distinct aspects.

The micro-company regime in Romania was subject to several important changes over the years. First of all, and probably the most prominent trait of this business entity regarded the annual income limit which was under 100,000 Euros. Another condition which had to be fulfilled in order to open a micro company in Romania concerned the number of employees that had to be between one and nine.

The share capital had to belong to other entities, but not the state or the local authorities. Businesses covering the banking, insurance, gambling or the capital markets field were not qualified for this scheme.

Another stipulation regarded the fact that the Romanian microenterprises could not have their social capital owned by a shareholder/associate who had over 250 employees. These were the most important particularities describing this specific class of companies until the beginning of 2013.

The regime for the micro company in 2024 remains the same in some aspects, such as ownership (to be owned by individuals, not by the state or local administrative units). The other conditions are the following:

- have a total turnover of no more than 500,000 euros (the equivalent in lei);

- the authorized capital is held by individuals, it is not state-owned or owned by territorial administrative units;

- it is not under litigation or undergoing the winding-up process;

- has at least one full-time employee;

- the shareholders who own (directly or indirectly) more than 25% of the shares or voting rights in the company are not shareholders in another micro-company.

Our team can give you complete details about all the applicable conditions for the micro-company regime in 2024.

Question: What is the tax regime for a micro company opened in Romania?

Answer: The beginning of 2023 brought several radical changes for the Romanian microenterprises regime; these shifts altered the overall perspective and introduced new regulations which call for a different approach. Up until the end of 2012, Romanian microenterprises had quite a specific fiscal status that generally provided some substantial benefits for taxpayers. Until early 2013, if anyone had been interested to open a Romanian micro company, he would have enjoyed the optional taxation regime applying to these types of companies. This functioned as an advantageous feature and guaranteed the opportunity to pick from two different fiscal alternatives, the owner of the business could either pay 3% of the income or the regular 16% of the profit, as any normal Romanian company.

Nowadays, if willing to open a Romanian micro company, everyone should be aware of the significant changes that took place at the taxation level.

The condition of having between one and nine employees was also excluded. This means that micro companies are not conditioned per se to have at least one full-time employee, however, if they do not have at least one employee, they will not be able to apply the 1% turnover tax regime. The experts at our law firm in Romania can give you more details on employment.

The tax rates for the micro-company regime are the following:

- 1% for companies with a revenue that does not exceed EUR 60,000 and do not engage in the list of activities for which the 3% rate applies;

- 3% for companies with revenue that exceeds EUR 60,000 or those that carry out certain types of activities in business sectors such as IT, HoReCa, and certain legal or medical business activities.

It should be pointed out that the 500,000 EUR threshold for qualification is calculated by taking into account the income of the Romanian legal entity, along with the income of companies that are related to it (if applicable).

The withholding tax on dividends has also changed in 2023, from 5% to 8%.

Companies that derive more than 20% of their income from consulting and management services cannot opt for the micro-company regime. Companies operating in other fields (banking, insurance, reinsurance, gambling, etc.) are also prevented from doing so.

Depending on the company’s activities, the special micro-company regime can be an advantageous one. In some cases, businesses that have not recorded a large profit but have made certain investments may choose to switch to the profits tax of 16% as it can be more convenient. One of our attorneys in Romania can provide investors with more details on this subject. They can also assist you if you need VAT registration services in Romania. A micro-company is expected to start complying with the value-added tax registration, reporting and payment regulations once it reached the reporting threshold of 300,000 lei.

Our Romanian lawyers can provide more details on how to change the taxation level if you hire more employees or reduce their number.

We invite you to watch a video about the Romanian micro company:

Micro companies are allowed to offer sponsorships, and this can result in a reduction of the due taxes for the quarter in which the said sponsorship is made. The regime under which these types of companies could offer sponsorships was changed to include more types of non-profit entities that may receive aid. However, a micro-company that wishes to make a sponsorship (and benefit from the tax reduction of approximately 20%) must first check if the NGO is included in the list approved by the National Agency for Fiscal Administration.

A micro-company is not subject to mandatory auditing in many cases, however, there are situations during which this type of company may fill two of the three conditions for audit obligations. Our team lists these general conditions below:

- total assets of 3,650,000 EUR;

- net turnover of 7,300,000 EUR;

- average number of employees during the tax year: 50.

As noted, these are the general conditions which, fulfilled by companies of any type lead to mandatory auditing obligations. However, one should note that the obligations only arise when a said legal entity exceeds these limits for two consecutive tax years. Given the fact that a micro-company has a turnover of no more than 1 million euros (this is below the aforementioned condition of 32,000,000 lei), it will only qualify for mandatory auditing if it exceeds the remaining two limits.

Those interested in knowing more about mandatory audits for companies can reach out to the tax experts at our Romanian law firm.

If you are interested in buying land in Romania, our lawyers can assist you throughout the pre-purchase and post-purchase stages. We will assist you with property due diligence purposes by enlisting the needed experts and will verify the property documents and the sale/purchase agreement. You can contact us for more information about your rights to buy and own land in Romania.

Accounting compliance, avoiding penalties

Micro-companies can be subject to the applicable penalties for failure to observe the provisions of the accounting law. The fines vary and some of these are listed below by our lawyers:

- failure to record any assets and liabilities as well as the performance of all economic and financial operations is sanctioned with a fine from 1,000 lei to 10,000 lei; the fine is applicable for the tax year during which the omission was made;

- failure to comply with the ongoing accounting principles for drawing up and keeping relevant accounting records, as well as registering them for the appropriate period and reconstructing lost or damaged documents is subject to a fine between 300 lei and 4,000 lei;

- not observing the requirements to draw up, file, and sign the documents required by the Ministry of Public Finance and its territorial units is subject to a fine between 1,000 lei and 3,000 lei;

- submitting the relevant statements that show that the entity in question did not engage in any activity, at least 30 days before the start of the chosen tax year is subject to a fine between 100 and 200 lei; newly incorporated companies in Romania are required to do so within 30 days after incorporation;

- submitting incorrect, incomplete or uncorrelated financial statements, including incorrect data for identifying the reporting entity is subject to a fine between 200 and 1,000 lei;

- a fine between 400 and 5,000 lei applies in the following cases: incorrect inventory, the company administrator’s noncompliance with preparing and signing the annual financial statements;

- a larger fine applies for failure to publish the consolidated annual financial statements by the parent company;

- fines apply for late filing according to the number of delayed days.

Please keep in mind that these are only some examples of applicable fines. Our attorneys in Romania can help you comply with all the requirements so that you may avoid these types of fines.

Question: What is the micro company for European funds?

Investors in Romania who wish to access European funds can open a micro company that qualifies for this purpose. The characteristics of this business form have been highlighted in the documentation issued by the European Commission. Below, our lawyers in Romania highlight some of the main traits of this type of company:

- the number of employees needs to be under ten: either 0 employees or a maximum number of 9 employees.

- the annual turnover needs to be below 2 million euros.

As far as the number of employees is concerned, it includes the following: the actual employees, the temporary employees, the owners who are also the administrators of the company, the partners who regularly provide services for the company and benefit from material remuneration or advantages. The total number of employees does not include interns or students who undergo their professional development and have corresponding contracts. It does not include employees who are on maternity or paternity leave.

The total number of employees for micro-companies that wish to access EU funds is calculated at the end of the most recent accounting period. Moreover, the turnover is calculated by excluding the value-added tax and other indirect taxes. Along with these thresholds, another important element is whether or not the micro-companies are autonomous.

One of our lawyers in Romania can provide investors with more details on the treatment of micro-companies for the purpose of accessing European funds.

Our lawyers can also help you with other matters, such as divorce in Romania. You can check with us if you meet the conditions for divorce, either by the court or administrative means or through a notary public. The procedure is easier when both parties agree to the separation, however, if an agreement cannot be reached, then the only option is to move forward with a court procedure.

These continuous transformations of the Romanian legal system obviously generate confusion that might evolve into future financial insecurities. Through our expert lawyers from Bucharest, we have always tried to minimize these possibilities of business failure, by skillfully advising our clients in their best interests. Our team is able to provide all necessary help and assistance throughout the process of micro company registration in Romania, indicating the most appropriate financial alternatives and guiding you to safer investing. Call us now for a free consultation, we are here to help.

Cristian Darie

Meet Cristian Darie, a committed lawyer at Darie, Manea & Associates skilled in national and international legal matters. Contact our firm for legal assistance.

View profile

Marcela Manea

Meet Marcela Manea, managing partner at Darie, Manea & Associates, with over 7 years of practice guiding clients through complex legal matters in Romania.

View profile

Adriana Tugui

Adriana Tugui, managing partner at Darie, Manea & Associates, brings over 14 years of legal experience advising clients across Romanian law.

View profile

Laurentia Gheorghe

Laurentia Gheorghe is a senior lawyer leading our Criminal Law and Business Crime Department in Romania. Contact Darie, Manea & Associates for criminal defense.

View profile