Value-added tax is an indirect tax imposed on the provision of certain types of goods and services.

Romania, like other countries, implements a standard VAT rate, along with several reduced rates for certain categories of goods and services.

VAT registration in Romania is possible before and after the commencement of the economic activity.

Businessmen who need VAT Registration services in Romania can rely on our team of lawyers. We invite you to read below important details below about this procedure.

Romanian VAT registration for foreign companies

A taxable person who has established his business outside Romania but is established through a fixed registered office must apply for registration for VAT purposes under the terms of the Tax Code.

With regard to taxable persons not established in Romania nor registered for VAT purposes in Romania, they will require registration for VAT purposes to the competent authorities for operations that are tax-deductible, conducted in Romania, other than transport services and services ancillary thereto, prior to the operations, except for the case that the person liable to pay tax is the beneficiary.

Foreign businessmen who want to obtain a Romania VAT number should know that for registration of legal entities in the Trade Register when the predicted turnover will exceed the 300,000 lei threshold, the documentation required for VAT registration in Romania is submitted on the same day as filing the documentation with the Trade Register.

Foreign companies will appoint a local tax representative who will help them meet the VAT registration requirements.

Working with a tax specialist is always advisable, however, for foreign companies, this is highly recommended for the purpose of filing a complete and correct VAT registration request with the authorities.

Our lawyers in Romania can help you obtain a Romanian VAT number in 2025 for your company.

| Quick Facts | |

|---|---|

| We offer VAT registration services |

Yes |

|

Standard rate |

19% |

|

Lower rates |

9% and 5% |

| Who needs VAT registration |

locally registered taxpersons with an annual turnover over RON 300,000 |

| Time frame for registration | Approximately 3 working days |

| VAT for real estate transactions |

9% starting with January 2024 in most cases |

| Exemptions available |

Education and medical services, veterinary services, activities carried our by certain non-profit associations, public radio, television, postal services activities, trade union organizations, and others |

| Period for filing | Monthly VAT returns submission Quarterly submissions and payments apply in case of taxable persons with an annual turnover below EUR 100,000 |

| VAT returns support | Upon request |

| VAT refund | Yes, for VAT-registered taxable persons, as per the provisions set forth in the Fiscal Code |

| Local tax agent required | Advisable |

| Voluntary VAT registration | Possible even if the legal entity does not exceed the prescribed threshold. |

|

VAT registration for foreign entities |

Mandatory in the case of foreign companies involved in the intra-community sale of acquisition of goods, and in other cases. |

|

Registration during the tax year |

Yes, if the company exceeds the threshold. |

| VAT return filing deadline | The 25th day, the next month after the month in which the return period ends. |

| VAT consolidation |

Permitted under certain conditions for related parties that qualify for this purpose. |

| VAT on invoice |

Mandatory |

| Invoicing system |

An electronic invoicing system will be implemented starting in 2024. |

| Reverse VAT charge |

For certain categories of goods; both parties need to be registered for VAT purposes. |

| Tailored VAT registration and compliance services in Romania |

Our local team of tax specialists can answer any questions related to VAT, and assist during registration. |

| Other tax services we provide | General tax law and annual filing compliance, taxation optimization, double taxation issues, and more. |

| When to contact us |

Before or after the completion of the company formation procedure, for complete assistance during the mandatory tax registrations. |

| Examples of services taxed at the 5% rate | Books, magazines, newspapers, and others |

|

Examples of services taxed at the 9% rate |

Human and veterinary use medicines, drinking water and irrigation water delivery, services related to access to fairs, recreational and amusement parks, sporting events, and others. |

|

Examples of services that are no longer subject to a reduced rate starting with 2024 |

Sugary foods (according to sugar content), non-alcoholic beer, the transport of passengers for tourism/leisure purposes, access to sporting facilities that fall under certain NACE codes. |

| Intra-community VAT | The company must register for a special VAT code for intra-community transactions when their value exceeds EUR 10,000 (the equivalent in lei). |

| Intra-community VAT compliance |

Concerned companies need to submit additional declarations if they engage in intra-community deliveries/supplies/acquisitions. Our team can give you more details. |

| Voluntary VAT deregistration |

Via a special form submitted to the authorities. |

| Automatic VAT deregistration for failure to file the returns |

If the company did not submit the VAT returns for 6 consecutive months or two calendar trimesters (when its VAT period is a calendar trimester). |

| Other situations for automatic VAT deregistration |

Take place when the company is declared inactive, or temporarily inactive, the shareholders/administrators have certain crimes included on their criminal record, and in other cases. |

| When to contact us for VAT registration |

During company formation or immediately after |

| When to contact us for other tax solutions | As soon as you have specific questions concerning your tax liability in Romania. |

| Other services offered by our team |

Our team not only includes tax lawyers, but also real estate and immigration specialists, divorce lawyers, corporate and commercial lawyers, and others. |

VAT registration for a local company

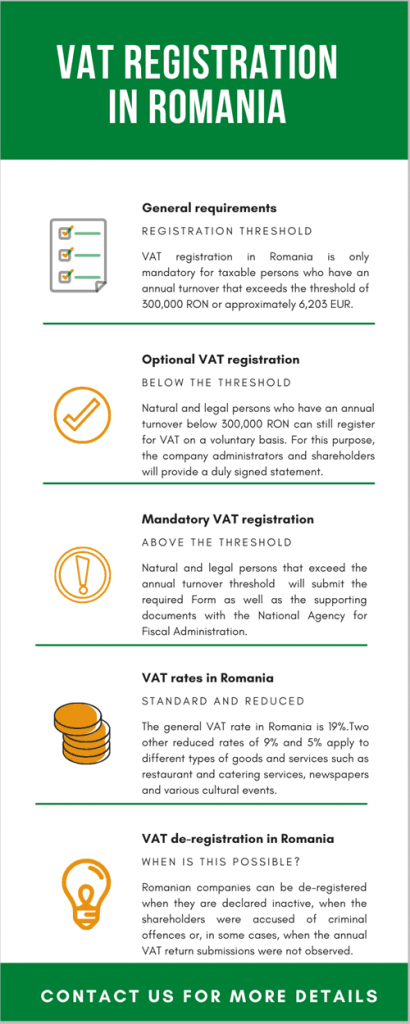

According to the Tax Code, the taxable person with business operations in Romania is required to register for VAT purposes in the following cases:

a) previous to the operations, if:

- he/she declares that will achieve a turnover that meets or exceeds the exemption threshold of 300,000 lei;

- he declares that turnover will be below the exemption threshold of 300,000 lei, but opts to register voluntarily;

b) when during a calendar year, it equals or exceeds the exemption threshold of 300,000 lei, within 10 days after the month in which the business recorded or exceeded the registration threshold;

c) when the turnover achieved during a calendar year is less than the exemption threshold of 300,000 lei, but opts to apply the normal tax regime;

d) when it carries out tax exemption operations and opts to tax these operations according to art. 141 para. (3) of the Tax Code.

Starting with 2020, commercial companies that apply for VAT registration, in the aforementioned conditions, are no longer subject to an analysis based on the criteria for financial risk assessment

However, the fiscal body will perform subsequent risk analyses for the legal entity, during the course of its activity.

The authorities can cancel the VAT registration in case of legal persons that present a high fiscal risk.

Taxpayers should know that the VAT registration application can be processed within 45 days for the submission of the request.

In practice, this term can be shorter, depending on the time the authorities need to evaluate the submitted documents.

Companies that choose to register for VAT after incorporation can expect a same-day registration, however, we do need to underline the fact that the authorities undertake to verify the submitted documents within 15 days.

The role of the taxable person registered for VAT purposes is reduced to that of a recipient of the tax, on account of the Ministry of Finance. This tax is not a cost for the respective taxable person, except for the costs that can arise for the purpose of fulfilling the administrative obligations.

The taxable person registered for VAT purposes must pay the difference between the amount of tax collected from its customers, applied either to the value or to the specific operations, as well as the deductible tax paid or owed by the respective taxpayer for the purchase of goods and services.

VAT is applied to specific operations, and not to gross profit. It is a tax that applies to final consumption.

If you are a business owner in Romania, SRL, or otherwise, our attorneys in Romania can help you with the VAT registration.

VAT registration steps in 2025

In order to obtain your Romania VAT number, you must complete and submit an application for registration found on NAFA’s official website, under the conditions and criteria set out in Order no. 17/2015 on establishing criteria for conditioning the registration for VAT purposes.

The form under which the taxable person requires re-registration for VAT purposes is form 099 “Application for VAT purposes according to art. 153 para. (9^1) b), d) of the Law no. 571/2003 on the Tax Code “. If such an application is not submitted within 180 days from the date of cancellation, the tax authorities will not approve any subsequent applications for registration for VAT purposes.

Foreign businessmen who want to obtain a Romania VAT number should know that for registration of legal entities in the Trade Register. When predicting overruns of the 300,000 lei threshold, the documentation required for VAT registration in Romania ( form 098 and form 088) is deposited on the same day as filing the documentation with the Trade Register.

However, a company that performs economic activities can opt to register for VAT after the registration in the Commercial Register, even if the threshold that obliges the company to register for VAT purposes is not met, by filing Forms 010 and 088 to the tax authorities.

The ascertainment of the conditions of registration for VAT purposes in Romania under art.153 of the Tax Code is carried out by the department responsible for tax registration based on information present in the financial semester/annual statements, statements and other documents filed by taxpayers.

These conditions, as stipulated by the fiscal authorities are the following:

- a) the legal person is not in a position to not do business in the space designated for headquarters and / or secondary offices or outside them;

- b) none of the managers and / or associates of the taxable person applying for registration for VAT purposes in Romania, nor the taxable person himself/herself applying for registration don’t hold in their tax record crimes and / or facts referred to in art. 2 para. (2) a) of the Government Ordinance no. 75/2001 on the organization and functioning of the tax record;

- c) the assessment, based on an analysis conducted by the tax authorities, of the intention and ability of taxable persons to carry out economic activities involving taxable transactions and / or exempted from VAT with rights to deductibility, as well as operations for which the place of delivery / provision is considered to be abroad if the tax would be deductible if these operations would take place in Romania.

Our team of Romanian lawyers can provide you with more details about these conditions.

If the taxpayer meets the evaluation criteria in part, the responsible department in assessing the intention and ability to conduct business invites the legal representative of the taxpayer to its headquarters.

If the taxpayer meets the evaluation criteria in part, the responsible department in assessing the intention and ability to conduct business invites the legal representative of the taxpayer to its headquarters.

If the latter does not provide the accurate and complete data and information required and doesn’t clarify the intention and ability of the taxable person to carry out economic activities involving ones for which the VAT applies, then the competent authority forwards the request for VAT registration to the competent regional fraud directorate.

This Directorate, upon the receipt of the complete documentation on the case, will be the final body that will issue the proposal to approve or refuse the registration for VAT purposes in Romania.

The request for VAT purposes registration ends with the decision to approve / reject the registration, once this decision is communicated to the taxable person.

VAT adjustment option

Taxable persons have the right to VAT adjustment when they apply for VAT registration after the commencement of their economic activities (by option).

Companies that request VAT registration as a result of exceeding the threshold can also apply for VAT adjustment within the legal term for this procedure (10 days following the date on which they reached or exceeded the registration threshold).

The following legal entities are entitled to the adjustment of the deductible tax:

a) the goods in stock, unused services and tangible fixed assets in course of execution, ascertained on the basis of inventory, at the time of switching to the regime, according to art. 304 of the Fiscal Code;

b) capital goods for which the deduction adjustment period did not expire, goods in the possession of the taxable person at the time of the transition to the normal tax regime, as per Art. 305 of the Fiscal Code;

c) tangible fixed assets which until December 31, 2015, were not considered capital goods, which were manufactured or purchased until January 1 2016 and which are not fully amortized at the time of switching to the normal tax regime, according to art. 306 of the Fiscal Code;

d) purchases of goods and services which are to be obtained, respectively for which the chargeability of the tax occurred according to art. 282 para. (2) lit. a) and b) of the Fiscal Code, before the date of transition to the normal tax regime and whose existence generates tax, respectively their delivery/performance, takes place after this date.

Our team of Romanian lawyers can give you more information about the adjustment of the value-added tax.

VAT registration annulment

The tax authorities may withdraw the registration of a person for VAT purposes in Romania in the following situations:

- a) if it is declared inactive;

- b) if entered into temporary inactivity, registered in the trade register;

- c) if the taxpayer’s associates or managers or the taxpayer hold in their tax record criminal tax offenses and / or other facts provided by the Law on the organization and functioning of the fiscal record.

- d) if there was no deposit of VAT return provided by the Tax Code, under certain conditions;

- e) if the tax returns filed for 6 consecutive months, for some persons, did not reveal the purchase of goods or services or supply of goods or services;

- f) if the taxpayer was not required, nor had the right to request such registration;

- g) for taxable persons requesting removal from the records of persons registered for VAT purposes in order to apply the special exemption regime provided by the Tax Code;

- h) if a company established in Romania subject to registration in the commercial register has no intention and ability to conduct economic activity.

Our Romanian lawyers can assist you if the company is included in one of these situations.

We invite you to watch a video on VAT registration in Romania:

I heard of the EU VAT number. What is this VAT number and do I need to register?

Answer: The intra-Community VAT number was introduced as a necessity since companies were burdened by futile administrative tools.

The intra-Community trade is standardized through this tax, which is applied to taxable entities selling goods and services across European countries’ borders. The most important categories of taxable transactions refer to the supply of goods made by a taxable person, acquisitions in a Member State of goods from another Member State, services provided by a taxable person and imports of goods from outside the European Union.

In order to register for an EU VAT number, business entities in Romania must register as an intra-Community trade operators. There is a set of documents that must be provided in order to complete this registration process. A response shall be provided by the fiscal authority within ten days of the application. These procedures are mandatory since any business entity which omitted to register with the Registry of Intra-Community Operators shall not be provided with a valid EU VAT number, under any circumstances.

The experts at our Romanian law firm can assist companies that perform intra-community acquisitions.

Is there any obligation to register for VAT for making intra-Community acquisitions?

Yes, according to the Tax Code, the following persons are required to apply for registration for VAT purposes:

- a taxable person established in Romania and non-taxable legal person established in Romania, which are not registered and are not required to register under Art. 153 of the Tax Code and are not already registered under the following paragraphs, performing a taxable intra-Community acquisition in Romania, before they make the purchase, if the purchase amount exceeds the threshold for intra-Community acquisitions in the calendar year in which the acquisition takes place;

- a taxable person who has established his/her business in Romania, unregistered and not required to register under art. 153, the previous paragraph or the next, when providing services in another Member State where the beneficiary of the service is a person liable to pay tax under the equivalent provisions of art. 150 para. (2) of the Member State’s legislation, before the service;

- a taxable person who has established his business in Romania, unregistered and not required to register under Art. 153 and that is not already registered under the previous or next paragraphs, if he/she receives services from a supplier, a taxable person established in another Member State, services for which he/she is liable to pay tax in Romania according to art. 150 para. (2), before receiving the services.

Before obtaining your Romania VAT number, you should know that a taxable person established in Romania that is not registered or required to register under Art. 153, as well as a non-taxable person established in Romania, can apply for registration if they make intra-Community acquisitions, in accordance with Art. 126 para. (6). Our Romanian lawyers can provide more details.

VAT rates in Romania in 2025

There are three main value-added tax rates applicable in Romania as of 1 January 2020. They are outlined below by our team of lawyers in Romania:

- 5%: this is one of the reduced rates applicable to certain foodstuffs (high-quality products and certain traditional products, for example), books, newspapers and periodicals;

- 9%: the other applicable reduced rate for pharmaceutical products, medical equipment for disabled individuals, foodstuffs that do not fall under the previous category (such as beverages, excluding alcoholic ones), ingredients used on the preparation of foodstuffs or water supplies; admission to cultural services, sporting events and amusement parks; the delivery of social housing as part of the social policy;

- 19%: the standard value-added tax rate in Romania, applicable to most types of goods and services such as domestic care services, bicycles, shoes and leather goods, clothing and household linen or hairdressing services, alcoholic beverages, among many others.

The VAT rate was changed for many types of goods and services starting on 1 January 2025. Our team highlights some important changes:

- the VAT rate for public transport is changed to the standard 19% rate for transport via historic trains or vehicles, cable stations, animal-powered vehicles, and boats;

- the VAT rate also increases to 19% for the delivery of goods considered to have a high-quality value, such as traditional or eco products;

- the delivery and installation of photovoltaic panels and other efficient heating systems is increased from 5% to 9%.

Investors and entrepreneurs in Romania can rely on our team of lawyers if they wish to be updated in due time.

VAT reporting and filing requirements

Companies that are VAT payers are subject to monthly or quarterly VAT submissions according to the company’s annual turnover.

These are filed electronically with the authorities before the 25th day of the month following the one for which the submission is made. The requirement is that the company owners submit two listed copies of the fiscal statements.

Taxable persons in Romania involved in imports and acquisitions may submit a request for the reimbursement of the value-added tax for purchases made within the EU. This is possible when the taxpayer has acquired certain types of goods and services from another EU member state. Examples of such goods include fuel, transport expenses, road taxes, accommodation, catering and restaurant services and others.

The submission is made with the National Agency for Fiscal Administration (NAFA). In order to be able to do so, the taxpayer needs to have an approved digital certificate and an account with the NAFA online portal.

Our lawyers in Romania can help you handle these pre-submission steps as well as submit the reimbursement request. In order to do so, the taxpayer is required to fill in form D318 and/or form D319 and our team can assist with the actual submission and the validation of the form.

2025 brings important changes to the reporting system in terms of the SAF-T standard (used for the electronic transfer of accounting and tax data from the legal entity to the state authorities). The reporting system has been implemented in stages and starting with 2025 it will become mandatory for all taxpayers.

Companies that are not registered for VAT purposes will submit the informative statement on a quarterly basis. Business owners should know that certain exemptions apply (such as for the authorized natural person or for the sole proprietorship) and a grace period will be in place initially. Our lawyers in Romania can give you more details upon request.

We can also assist those who wish to buy land in Romania or residential property. The purchase rules can differ according to nationality (EU vs. non-EU), and all foreign nationals are asked to apply for a special fiscal identification number, which will be instrumental in the land or property purchase. Our lawyers will give you more details about the requirements upon request.

Apart from corporate and personal taxation matters, we also assist clients who are interested in divorce in Romania. This is commonly lodged after the irretrievable breakdown of the marriage, however, we will assist you in filing a divorce claim irrespective of the grounds for divorce. We can also give you details about the condition in which a marriage is considered null.

Our law office can assist your company in obtaining the necessary documents requested for VAT registration in Romania. Call us now for a free consultation.

Cristian Darie

Meet Cristian Darie, a committed lawyer at Darie, Manea & Associates skilled in national and international legal matters. Contact our firm for legal assistance.

View profile

Marcela Manea

Meet Marcela Manea, managing partner at Darie, Manea & Associates, with over 7 years of practice guiding clients through complex legal matters in Romania.

View profile

Adriana Tugui

Adriana Tugui, managing partner at Darie, Manea & Associates, brings over 14 years of legal experience advising clients across Romanian law.

View profile

Laurentia Gheorghe

Laurentia Gheorghe is a senior lawyer leading our Criminal Law and Business Crime Department in Romania. Contact Darie, Manea & Associates for criminal defense.

View profile